IC No. 43 - Glitz and glamour

In Investment Commentary No. 43 – Glitz and Glamour, we discuss the rapid rise of gold. In our view, gold reflects dwindling confidence in the financial system. Central banks and private investors are supporting demand. We hold gold and are using the current high prices for selective rebalancing.

IC No. 43 - Glitz and glamour

The prominent role of gold dates back to the dawn of humanity. Early cultures worshipped the sun because it was considered the source of all life. With the colour of the sun, gold took on mystical significance early on. The lustre of gold has also been evident in jewellery throughout the centuries and continues to be so today. For us as investors, gold is above all a valuable portfolio component as a store of value and protection against inflation and crises.

With the spectacular rise in the price of gold, we now ask ourselves: What is gold signalling to us and what should be done?

What is gold trying to tell us?

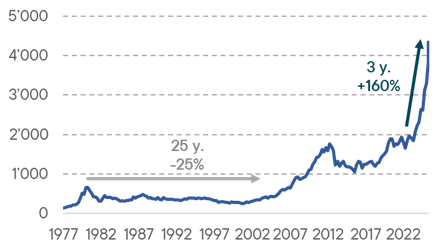

Gold price development in USD/ounce, 1977 - 2025

Preservation of value

Gold has not always been helpful as a hedge against inflation or loss of purchasing power. Over a 25-year period between 1980 and 2005, gold lost 25% of its value, even though the US dollar lost 55% of its purchasing power during the same period.[1] And the inflation rates of the last three years cannot explain the 160% increase in the price of gold since 2022.

Trust

In our view, a much stronger explanation for the rise in the price of gold can be found in the question of whether today's financial system and government debt are sustainable. The clear answer is no.

The United States in particular is causing great concern with its excessive government deficit. And we have come to expect nothing else from Europe. Only Switzerland, as we occasionally point out, offers a glimmer of hope.

Sustainable debt?

Government debt in % of GDP, 2001 - 2030

Confidence in the financial system is being further undermined by politics. There is currently a real risk that the US government will influence the decisions of the US Federal Reserve. This could further weaken the Federal Reserve's already fragile independence and also undermine its credibility as a result.

On a buying spree

Of course, one wonders who is driving up the price of gold. The answer is complex, but there are some interesting buyer groups: central banks have been net buyers of gold for many years. Apparently, paper money needs to be backed by gold in order to be credible!

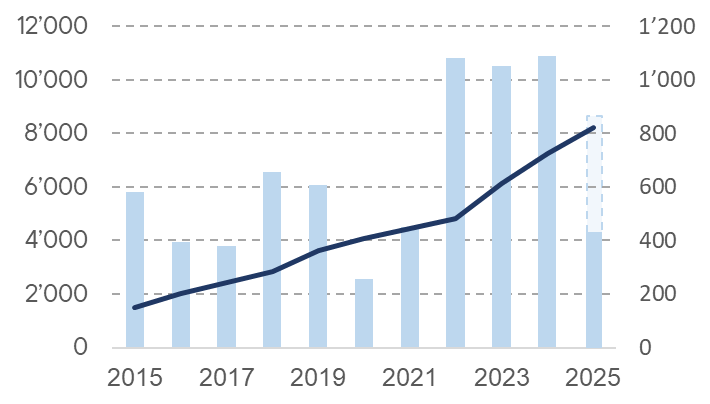

Central banks on a buying spree

Net gold purchases by central banks in tonnes, cumulative (left axis) and annual (right axis)

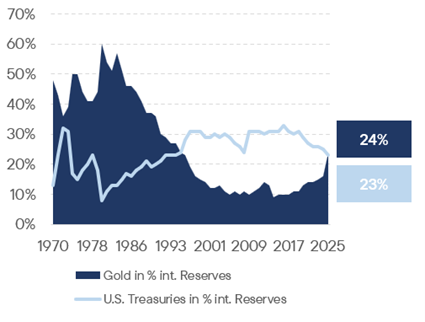

It is clear that countries such as China and Russia, but also many other countries, want to become less dependent on the US dollar. For the first time since 1996, central banks are once again holding more gold (24%) than US government bonds (23%) in their reserves.[2]

Anecdotally, our Swiss readers may recall that the Swiss National Bank sold a total of 1,300 tonnes of gold at an average price of CHF 520 per ounce between 2003 and 2005. This is unfortunate, as it means that the state coffers have lost around CHF 145 billion compared to today's prices.

Gold > US-Treasuries

Share of gold and US Treasuries in international central bank reserves, 1970–2025

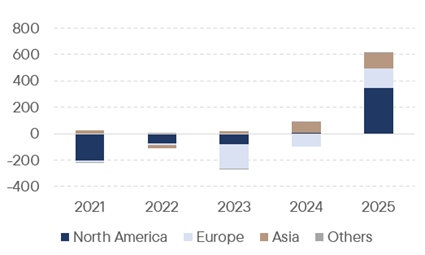

Another group of buyers are private investors. One striking trend is the sharp increase in buyers from the United States.

Private investors follow suit

Gold ETF inflows and outflows, regional, in tonnes

This is probably due to the political situation in the US, but also to rising national debt. In the land of the free, private ownership of gold was actually prohibited between 1933 and 1972.[3] The backlog is therefore large.

All in all, the spectacular rise in the price of gold appears to be a sign of dwindling confidence in the United States and other highly indebted countries. The manifold crises around the world are also contributing to this. Some analysts predict that the price of gold will rise to as much as USD 10,000 per ounce in the coming years.

Regardless of this, we wonder what makes gold productive beyond its role as a crisis currency? What benefits does gold offer beyond its value as a store of value?

What does the gold cube do?

The answer: not much. The world's total above-ground gold reserves amount to around 216,000 tonnes. This corresponds to a cube with an edge length of 22 metres. At today's prices, this cube is worth CHF 16,400 billion. For this enormous sum, you could buy the 200 largest listed companies in Switzerland seven times over, acquire all private residential property in Switzerland[4] and still have CHF 800 billion left over for other things. What would you choose in the long term? We also ask this question because shares are the better form of investment in the long term and gold has gained enormous importance as a store of value and temporary crisis currency due to price developments.

Equities shine brighter than gold

Annual returns 1900 - 2024, in USD

When will the time come to use the sharp rise in the price of gold to buy productive equity (shares)? So when should one consider rebalancing?

How much shine is appropriate in your portfolio?

Gold has once again become an indicatorof confidence. Real interest rates, the USD trend and ongoing central bank purchases explain the rise better than recent inflation. For investors, the important thing now is to translate this into allocation rules: what is a sensible long-term allocation – and when should we swap gold for equities?

When deciding how much gold should be held strategically in a portfolio, we have relied on the gold study by our advisory board member Prof. Dr Thorsten Hens. He considers gold quotas of 10% to 20% to be reasonable, although he prefers a gold quota of 10% in the longer term and advises regular rebalancing.[5]

Whereas in January 2023 you could get 16 Nestlé shares for one ounce of gold, today you can get 40 shares per ounce of gold. That's an increase of 60%. And while you could get 20 Novartis shares in January 2023, today you can get 32 Novartis shares for one ounce of gold, an increase of 30%.

Equities appear to be cheap compared to gold

Number of shares per ounce of gold

We believe the time has come to consider rebalancing the gold position in portfolios, not least because a higher proportion of productive capital can be purchased per ounce of gold.

Conclusion

Gold has been and remains an important component of portfolios, having increased enormously in value in recent years. The drivers behind this are a looming loss of confidence in the financial system, central banks seeking to become independent of the US dollar, and, last but not least, the manifold existing or looming crises. We continue to recommend holding gold but consider 10% to be a sensible long-term allocation in a portfolio. A temporary deviation from this (as is currently the case) may make sense and depends on individual risk tolerance. At current prices, a certain amount of rebalancing does not seem entirely unattractive.

Ausblick

History, and with it the capital markets, has always been full of crises. A sobering of expectations could cause the AI bubble to burst. Independent experts are talking about the biggest bubble of all time (17 times bigger than the dot-com bubble).[6] Prof. Dr Hens is also currently being interviewed about it daily. Accordingly, we are dedicating our next investment commentary to this topic, which we consider to be highly relevant (also in connection with gold as a crisis currency).

PC

Net gold purchases by global central banks, 1 January 2002 – 30 June 2025, in tonnes

Cumulative over the last 23 years

The geopolitical shifts in the world can also be seen in

physical gold reserves. It is striking that countries such as

Russia, China and Turkey have massively increased their

gold reserves, while European countries in particular have

sold off their gold reserves at far too low prices.

2002 to 2013: Western countries are the largest sellers of gold

2014 to 2025: Largest gold buyers are found in the Eastern Hemisphere

*Return 1972 - 2024 (after the end of the gold standard)

[1] Bureau of Labor Statistics

[2] Tavi Costa, Crescat Capital

[3] EBSCO, Executive Order 6102

[4] Handelszeitung, 28.04.2025

[6] Julien Garran, The Macrostrategy Partnership