IC No. 47 - Market assessment

Imagine you had spent the past few months on a media detox: no doomsday headlines, no negative news cycle, and no Eurovision Song Contest. You check in on your portfolio from time to time, and things look reassuringly steady. Then you learn that the United States and Israel have struck Iran, and that the Strait of Hormuz has been closed for weeks.

IC No. 47 - Market assessment

Puzzled, you scratch your head and wonder how the world is still turning. Understandably, you ask yourself: how can this be? Should markets not be in panic? Should global supply chains not be severely disrupted? Gas rationed? Markets in freefall? We did not go on a media detox ourselves — but the questions are entirely valid. With that in mind, we would like to take stock of recent market developments and offer an outlook.

The Obvious

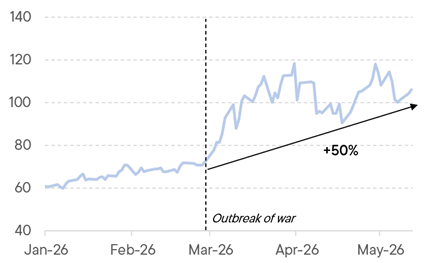

That a strike on Iran and the closure of the Strait of Hormuz would drive oil and energy prices higher is self-evident. The rise of +50% since early March is significant.

Rising Enery Costs

Oil price development in USD/barrel, year-to-date

Since energy is a key input factor for production costs and, by extension, inflation rates, a rise in short-term inflation expectations was a natural consequence. The impact is equally tangible for motorists and logistics companies, and hits lower-income households hardest.

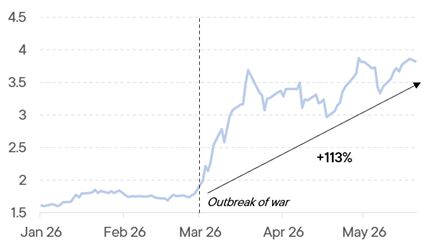

Rising Short-Term Inflation Expectations

1-year inflation swap Eurozone, in %, year-to-date

As a consequence of higher inflation expectations, yields have moved higher. 10-year US Treasuries are once again offering more than 4.5%. German Bund yields rose to 3.1%, while Swiss Confederation bond yields doubled to above 0.5%.

Rising Yields

10-year US Treasury yield in %, year-to-date

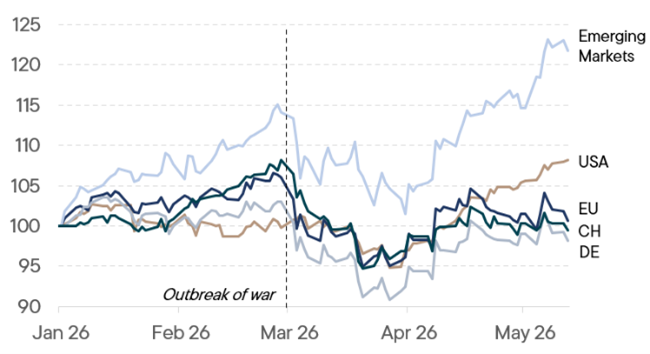

Equity markets fell by around 10% in the immediate aftermath of the strikes but recovered swiftly. This pattern is consistent with historical precedents from prior geopolitical conflicts and therefore comes as little surprise.[1] Notably, US equities have outperformed and left European markets - which initially lagged - clearly behind. The above-average performance of emerging markets has been the more unexpected development.

Global Market Performance

Returns of global markets, year-to-date, indexed in CHF

The Less Obvious

Investors had assumed that a US-Iran conflict would heighten global uncertainty and push gold prices further higher. The opposite occurred. Since 28 February 2026, the gold price has fallen by 11%.

Losing its Shine

Gold price development in USD/oz, year-to-date

We nonetheless continue to view gold as an important portfolio building block. Elevated debt levels globally, potential dislocations in the private credit market[2] and the long-term structural debasement of money remain compelling arguments for maintaining gold as a portfolio allocation. We consider a long-term strategic weight of around 10% to be appropriate.[3]

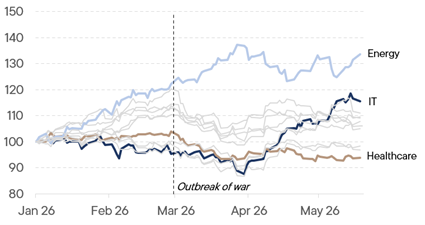

Looking more closely at equity markets, a sector-level perspective is always instructive. The outperformance of the energy sector is unsurprising. The key question going forward is whether energy prices remain elevated - sustained by a geopolitical risk premium - or whether, once the Strait of Hormuz reopens, energy reverts to even lower levels and valuations correct accordingly. In stark contrast to energy, healthcare has been the least sought-after sector year-to-date.

Sector Performance

MSCI World sectors, year-to-date, indexed in USD

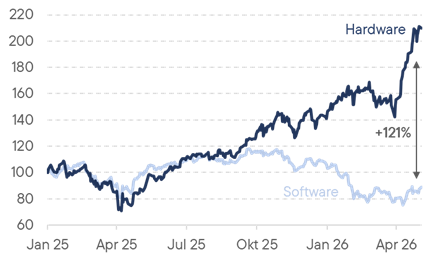

The IT sector also stands out positively, having staged an impressive rally particularly since late March. A more granular look at sub-sectors is warranted here. The divergence in performance between traditional software companies and the AI infrastructure universe - which we highlighted in our last commentary No. 46, "A Wall of Worries", has accelerated further.

AI on Steroids

Semiconductor index, S&P Software index, since 2025, in USD

Companies operating in the field of artificial intelligence - and in particular those providing the underlying infrastructure — are booming. Amazon, Microsoft, Alphabet and Meta alone announced a combined capital expenditure commitment for 2026 of approximately USD 700 billion.[4] Staggering sums. Experts argue that the so-called token explosion is still in its early stages. A token is the unit a large language model uses to read or generate text. 100 tokens correspond to roughly 75 words.[5] The total body of human-generated text available for training AI models is estimated at around 300 trillion tokens.[6]

In addition, the ongoing use of AI applications consumes tokens with every interaction, further amplifying demand for compute. According to experts, the exponential growth in token processing and AI-generated output is only just beginning. Companies at the forefront of AI infrastructure are accordingly in high demand.

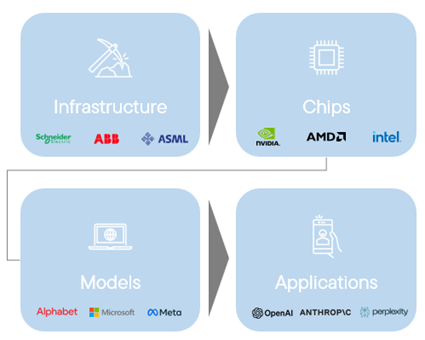

The AI Value Chain

Key companies across the AI value chain

The AI boom is no longer confined to technology equities. It is increasingly driving energy and infrastructure markets as well. AI data centers already account for more than 4% of US electricity consumption; by 2030, this share is expected to double or even triple.[7]

Recent headlines have been dominated by the AI data centres Colossus 1 and Colossus 2, operated by SpaceX/xAI. Colossus 1 comprises over 220,000 Nvidia chips and around 300 megawatts of compute capacity. xAI recently concluded a landmark deal with Anthropic, estimated to be worth approximately USD 5 billion per year - making it one of the largest AI infrastructure deals ever struck.[8] In parallel, Musk is already building Colossus 2, a next-generation supercluster expected to eventually house over 550,000 Nvidia chips and reach more than one gigawatt of capacity.

Capital markets, too, remain firmly in the grip of the AI theme. OpenAI (valued at USD 852 billion[9]) and Anthropic (valued at USD 350 billion[10]) are both preparing for initial public offerings. Alphabet's trajectory deserves particular mention. Regarded just a year ago as a potential AI laggard, Alphabet saw its market capitalization surge by approximately 160% over twelve months. A significant driver was not its core operating business, but rather the revaluation of its stake in Anthropic. Alphabet holds approximately 14% of Anthropic; nearly half of its record first-quarter 2026 profit was attributable to this revaluation.[11]

Prominent investors are also repositioning. Bill Ackman, through Pershing Square, has built a Microsoft position of approximately USD 2 billion, reflecting a high conviction bet on the company's central role in the AI ecosystem through Azure and the OpenAI partnership.[12]

The Future Obvious

Markets are thinking well ahead and pricing in an imminent resolution of the US-Iran conflict. Any report that supports this expectation triggers sharp rallies, particularly in a somewhat depressed European market. A resolution of the conflict could bring familiar market patterns back to the fore: Gradually declining inflation expectations and supportive global economic data. In this context, a sensible portfolio positioning may constitute a triage of:

• Technology companies with a focus on AI and AI infrastructure

• Broad global market exposure to capture global growth

• Positions in markets with catch-up potential, particularly in Switzerland and Europe

Despite all the challenges, the global economy appears to be more agile and resilient than one might think. The same holds true for capital markets.

PC

[1] Brune, Amelie and Hens, The War Puzzle: Contradictory Effects of International Conflicts on Stock Markets

[2] Financial Times, 12 March 2026

[3] Hens & Amstein, Gold for Long-Term Wealth Accumulation: A Financial Economics Analysis

[4] Annual reports Amazon, Microsoft, Alphabet, Meta

[5] OpenAI Help Center

[6] Epoch AI Blog

[7] American Public Power Association

[8] Wall Street Journal

[9] OpenAI press release 31 March 2026

[10] Reuters, Februar 2026

[11] Fortune, IEEE ComSoc Technology Blog

[12] Pershing Square Holdings - Investor Updates