IC No. 46 - Wall of worries

Sometimes it feels as if Hermes, the messenger of the Greek gods, were personally rushing through the world of finance, bringing news of looming trade conflicts, political upheavals, and geopolitical tensions, always with the greatest drama, as if the worst were just about to happen.

IC No. 46 - Wall of worries

And yet, as in the ancient myths, reality often appears far more composed. Since the election of Donald Trump and the introduction of tariffs, the markets have once again proven that short-term fears can hardly stop long-term growth.

Just as Hermes’ messages were at times somewhat exaggerated, market participants too tend to perceive risks as louder and larger than they actually turn out to be. The markets remind us: worries pile up, but they are rarely insurmountable.

The media as modern divine messengers

The global stock market has risen by +14.2% since Trump's election on November 5, 2024, up to today. Since the tariff dilemma on April 1, 2025, it has gained +12.4%. Year-to-date in 2026, it's up +1.6% (in CHF).

Facts, facts, facts

The good news is that it pays to focus on facts and ignore sensational opinions. Looking ahead, the economic outlook appears solid.

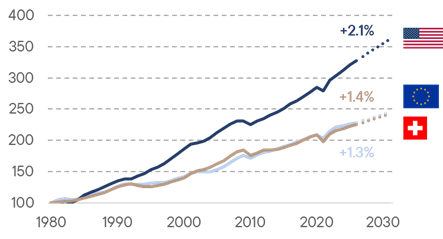

Growth, growth, growth

Real GDP growth: Switzerland, USA, Europe, in %

The International Monetary Fund (IMF) expects real GDP growth this year of +2.1% for the U.S., +1.4% for Europe, and +1.3% for Switzerland.[1] The interest rate environment also supports this favorable outlook, with advantageous financing conditions.

Money is becoming cheap

Interest rates of leading central banks: CH, US, EU, in %

Central banks are lowering interest rates not because of recession fears, but because of declining inflation amid a still solid economic backdrop.

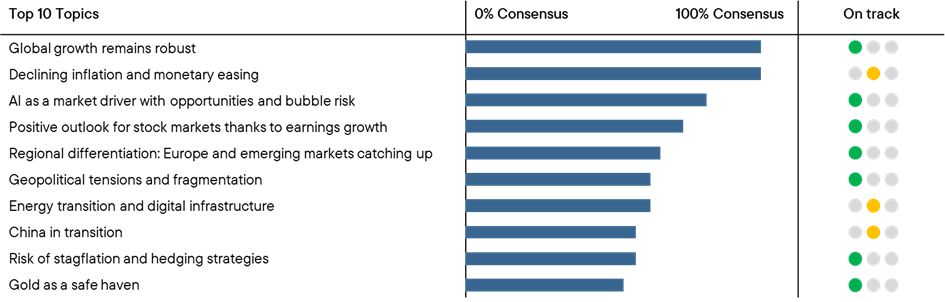

Everything on track?

Although we are still in the first quarter of the year, we thought it would be worthwhile to revisit the market forecasts from our IC No. 45 – Outlook of Outlooks 2026 and make an initial assessment. To keep things simple, we are using a traffic light system on the right-hand side of the following chart to present our evaluation, without going into complex analyses. All in all, the year so far appears to be unfolding largely as many market participants had anticipated.

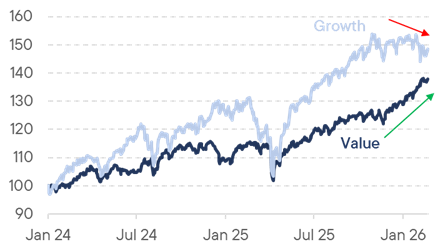

Watch closely

An interesting observation from our perspective is the development of expensively valued growth stocks (MSCI Growth) compared to cheaper value stocks (MSCI Value). After technology focused growth stocks performed better in 2024 and 2025, they have been outperformed this year by value stocks, which are more dominated by energy and industrial companies.

Growth versus Value

MSCI Growth vs. MSCI Value Index, since 2024, in USD

The shown shift between growth and value stocks could reflect a deeper break in the market: a trend toward investments in areas unaffected by AI disruption and which also have lower valuation levels. The market speaks of the HALO effect[2]: capital intensity is becoming respectable again.

Of course, in this context, we must talk about «Claude» and developments in the field of artificial intelligence.

In mid-January, software stocks lost approximately $830 billion in value in just seven days — roughly equivalent to Switzerland’s GDP. The trigger was the introduction of new AI agents from Anthropic. These agents operate autonomously, complete entire tasks rather than merely assisting, and are compensated per result instead of per user. Consequently, companies require fewer software licenses and less personnel, putting pressure on the classic SaaS model.[3]

With another release, Anthropic introduced «Claude Code Security», an AI tool that not only scans program code for known patterns but also understands context. With Claude Opus 4.6, over 500 real vulnerabilities in open-source projects were identified.[4] Investors reacted nervously: CrowdStrike -8.0%, Cloudflare -8.1%, Okta -9.2%. Investors fear that AI will partially replace classic security tools and put margins under pressure.[5]

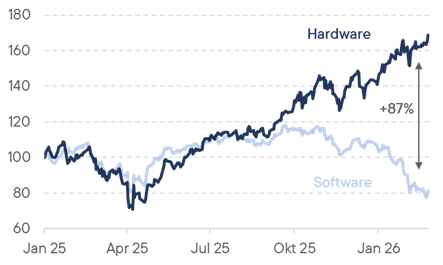

Investors are also taking divergent approaches within the technology sector. Companies building the physical infrastructure for artificial intelligence are preferred over providers that primarily offer AI as a function in existing applications. Thus, Nvidia's recently published record results with annual revenue of $216 billion exemplify this ongoing trend.[6]

Hardware versus Software

Semiconductors Index, S&P Software Index, since 2025, in USD

We believe that these developments will accelerate, and that artificial intelligence will render entire business models obsolete. It appears that these changes are occurring faster than anticipated.

Margin of safety > margin of hope

The increasing demand for safety among market participants is also reflected in the solid year-to-date performance of the Swiss stock market, the SMI, which is up 5.4%. In contrast, the Nasdaq has declined by 2.9% since the beginning of the year (in CHF). Similarly, the Swiss franc continues to strengthen against the US dollar, rising 2.6% year-to-date.

In an overall stable yet dynamic market environment, investors continue to feel comfortable with an allocation to gold. Gold is currently enhancing the margin of safety within portfolios. This remains true especially in light of geopolitical tensions (e.g., US/Iran), ongoing dollar weakness, and a still somewhat unsettled investor base.

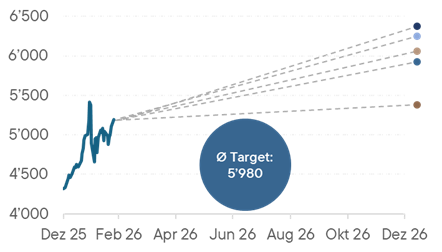

Looking at the 2026 price targets issued by major banks such as UBS, Goldman Sachs, JP Morgan, Deutsche Bank, and Société Générale, gold’s upward trajectory appears far from over. For an ounce of gold, the average price target by the end of 2026 is just under $6,000.

Gold price on track

YTD Performance and year-end price targets, in USD/ounce

Conclusion

Even if it sounds dull: remain invested, preferably in real, tangible assets that offer a higher margin of safety and a lower margin of hope.

PC

[1] World Economic Outlook, IMF.org, October 2025

[2] The HALO effect: Heavy Assets, Low Obsolescence in the AI era, Goldman Sachs Research, 24.02.2026

[3] The $830 Billion Wake-Up Call: How Claude Just “Murdered” the Old Software Industry, Medium, 17.02.2026

[4] Making frontier cybersecurity capabilities available to defenders, Anthropic, 20.02.2026

[5] Claude Code Security Causes A SaaS-pocalypse In Cybersecurity, Forrester, 23.02.2026

[6] Nvidia investor presentation Q4 FY26, 25.02.2026